Aký je rozvoj vedy a výskumu? = just for your information because no publisher in SR wanted my articles to be seen and understood by public.

Aká je úloha štátnych rozpočtov jednotlivých krajín? Predsa pokryť náklady spojené s fungovaním a zabezpečením potrieb štátu. Výdavky do vzdelávania, vedy, výskumu a vývoja by mali byť samozrejmosťou každého štátu, pokiaľ chce prichádzať s novými inovačnými technológiami a produktami. To si tiež vyžaduje stimulovať, motivovať a odmeňovať vedeckých pracovníkov pôsobiacich v oblasti školstva.

Pokiaľ sa pozrieme na výdavky na vzdelanie v štátnom rozpočte v Slovenskej republike, tak podľa údajov z OECD predstavujú čiastku 14,546 mln EUR v roku 2014, v porovnaní s rokom 2006 je badateľný nárast o 514, 90% a oproti roku 2013 sa výdavky zvýšili o 73,08%. Načŕta sa otázka, počet vysokých, stredných škôl k počtu obyvateľov. Ako sa starajú školy o svojich študentov? Ako si vážia školy študenta? Ako školy pristupujú k poskytovaní vzdelávania študentom, a ako študenti pristupujú k získavaniu a nadobúdavaniu nových poznatkov a informácií? Sú učitelia, pedagogickí pracovníci spravodlivo odmeňovaní? Je potrebné zmeniť systém na SR? Jednoznačná odpoveď.

Dok1 Zdroj: Autorove spracovanie na základe údajov z OECD, 2013

Pokiaľ sa pozrieme na výdavky na vzdelanie v štátnom rozpočte v Českej republike, tak podľa údajov z OECD, predstavujú čiastku 344,168 mln Czech koruna v roku 2014, v porovnaní s rokom 2005 je značný nárast o 339,98% a oproti roku 2013 sa výdavky zvýšili o 34 mln czech koruna. Vidíme odliv mozgov, predovšetkým zo SR do tejto susedskej krajiny, aj z dôvodu nízkej jazykovej bariéry. Výdavky na vzdelanie v poľsku dosiahli sumu vo výške 257,2 mln zlotych v roku 2013.

Zdroj Zdroj: Autorove spracovanie na základe údajov z OECD, 2013

V maďarsku je situácia, že vládne výdavky do vzdelávania tvoria sumu vo výške 1194,9 mln forintov v roku 2013, je značný nárast o 870,84% oproti roku 2007, a nárast o 884,2 mln forintov oproti roku 2012.

Zdroj: Autorove spracovanie na základe údajov z OECD, 2013 V nemecku vládne výdavky do vzdelávania sú vo výške 313,511 mln EUR v roku 2014, je značný pokles o 49,98% oproti roku 2005, a nárast o 67 mln EUR oproti roku 2013.

Dok4 Zdroj: Autorove spracovanie na základe údajov z OECD, 2013 Situácia vo Veľkej Británii je nasledovná, výdavky na vzdelávanie sú vo výške 36,2 mln pounds in 2013, na druhej strane je značný pokles o 29,49% v roku 2006.

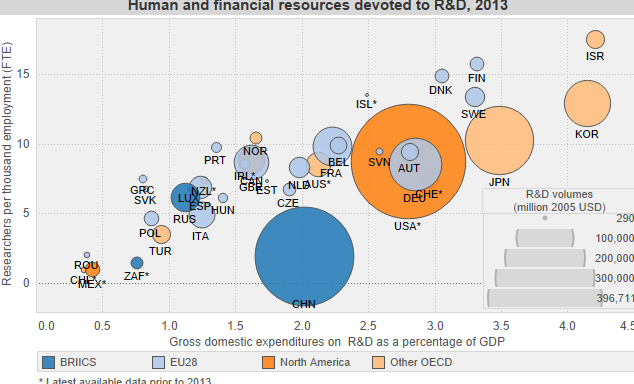

Podiel HDP do výskumu Z pohľadu ľudských a finančných zdrojov v porovnaní podiel HDP, spracované OECD, je veda a výskum v roku 2013 situovaná z geografického hľadiska v krajinách BRIICS, Severná Amerika, Japonsko, Kórea. Načŕta sa otázka, koľko dávajú jednotlivé krajiny do rozvoja vedy a výskumu z podielu HDP. Pokiaľ sa pozrieme na štáty V4, tak česká republika investuje 1,92% z HDP, maďarsko 1,41%, poľsko 0,87% a slovenská republika len 0,83% z HDP investuje na podporu vedy a výskumu. Na druhej strane, je potrebné spomenúť krajiny, ktoré si uvedomujú ako investície do vedy a výskumu dokážu priniesť inovácie, start-upy, patenty. Napríklad Izrael investuje do vedy a výskumu 4,21% z HDP, 4,15% z HDP investuje Kórea, Japonsko 3,47% z HDP, Fínsko 3,31% z HDP, Švédsko 3,3% z HDP, Dánsko 3,06% z HDP, Nemecko 2,85% podľa údajov z OECD, dostupný dáta z roku 2013.

Patent, predstavuje ochranný dokument, udelený štátom a dáva majiteľovi právo zakázať inej osobe, aby pri svojej akejkoľvek činnosti vyrábala alebo dávala na trhu vynález bez súhlasu majiteľa. Inak povedané, pokiaľ nejaký človek vyvinie unikátny výrobok, proces, postup, tak si ho dá patentovať, že je to jeho 100% vlastníctvo. Z geografického pohľadu, v roku 2013 podľa OECD, 1785 je evidovaných patentov v Číne, v Európskej Únii je to 14 161.6 patentov, v Nemecku je registrovaných 5 465.2 patentov, v Japonsku je to 15 970.1 patentov, v Kórei je to 3 154.4, v USA je zaevidovaných 14 606.2 patentov, v UK je to 1 769.9. V slovenskej republike je registrovaných 11,2 patentov. Je potrebné dodať, že poznáme 3 veľké patentové úrady: the European Patent Office (EPO), the Japan Patent Office (JPO) a the United States Patent and Trademark Office (USPTO). Daný indikátor je vypočítaný podľa krajiny bydliska, dátumu.

Aký je počet vedeckých pracovníkov resp. ľudí pracujúcich v oblasti vedy a výskumu? V Číne sa oblasti vedy a výskumu venuje 12.777 ľudí, v Dánsku je to 14.863 ľudí, vo Fínsku 15.681, v Kórei 12.840, vo Švédsku je to 13.323, v Nórsku je to 10.420 ľudí. Francúzsko reprezentuje 9.806 vedeckých pracovníkov v roku 2013 podľa dostupných dát z OECD.

(C) All Rights Reserved, Not published in any journal or newspaper yet, feel free to contact me directly in order to sign lucrative contract with MY conditions.

You must be logged in to post a comment.